Wars have historically been one of the biggest drivers of major jumps in US government debt.

The war Between the States in the 1860s was the first true explosion: federal debt rose from about $65 million in 1860 to roughly $2.7 billion after the war—an increase of over 4,000%.

(The percentage growth is so large because the debt was starting from such a low base, with President Andrew Jackson having completely eliminated it in 1835. Likewise, the percentage growth during later conflicts is smaller because they began from a much larger debt base.)

World War I produced another huge leap, taking debt from about $2.9 billion in 1914 to about $25 billion by 1920—up roughly 760%.

World War II was even larger in nominal terms, pushing debt from about $51 billion in 1940 to about $260 billion after the war—an increase of about 410%.

The Vietnam War saw US government debt rise from about $317 billion in 1965 to about $533 billion in 1975—up roughly 68%.

Using the best available estimates, the Afghanistan War added costs roughly equal to 59% of the federal debt outstanding when it began, while the 2003 Iraq War added costs roughly equal to 47%.

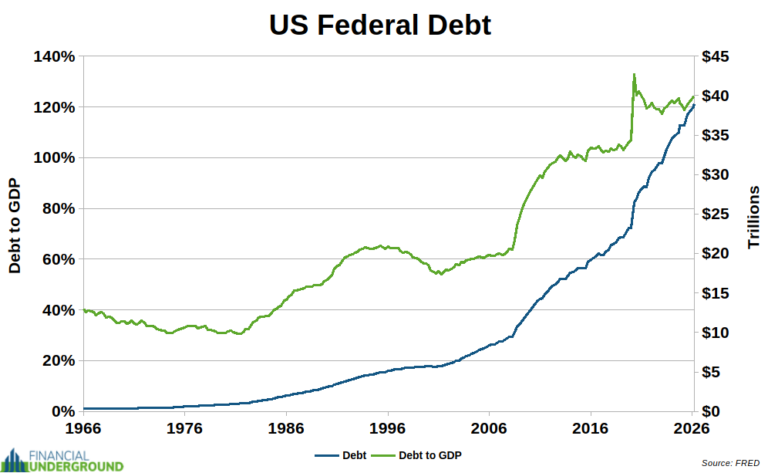

We are now well into the third month of the Iran war. US federal debt stood at roughly $38.7 trillion when the war began and has already climbed past $39.2 trillion. Where will it be when the war ends? Nobody knows, of course, but I think we can say with confidence that it will be meaningfully higher.

Indeed, war = Inflation, but there is an intermediate step in the process: debt.

War spending is financed largely through debt, which is then, in large part, bought by the central bank with currency it creates out of thin air.

A more accurate equation, therefore, is:

War = Debt = Inflation

That is how the Iran war is turbocharging the US government’s debt spiral and accelerating its ever-increasing currency debasement, which was already nearing a crisis point even before taking into account the compounding effects of the war.

But that is not all.

Another likely casualty of the Iran war is the petrodollar system, which is essentially a protection racket for the large oil-producing countries in the Middle East aligned with the US, such as Saudi Arabia, Kuwait, the United Arab Emirates, Bahrain, and Qatar.

The concept is simple. The US military “protects” these countries in exchange for their agreement to denominate oil sales in US dollars and recycle the proceeds into the US Treasury market, thereby supporting the dollar and helping keep interest rates lower than they otherwise would be.

The petrodollar system has been a massive prop for the US dollar ever since Nixon severed the dollar’s last link to gold in 1971.

However, that system is now crumbling before our eyes.

The Iran war is a stark illustration of the limits of US military power and its inability to provide the protection the oil-rich Gulf Arab states believed they had. Iran has shown that it is the new sheriff in town and that US promises of protection are not only worthless but counterproductive, as the US presence invites uncontrolled instability into their regimes.

And with Hormuz closed and oil infrastructure damaged, far less of their oil is being sold and, therefore, far less is being recycled back into the Treasury market. That is another headwind for US Treasuries.

Not only is there less demand for Treasuries from petrodollar recycling by Persian Gulf oil producers, but there is also potential selling pressure.

The United Arab Emirates has floated the idea of selling some of its Treasury reserves, which make up a large portion of its $285 billion in foreign reserves, to offset the loss of oil revenue. Rather than sell Treasuries and risk unsettling the bond market, it requested a currency swap line. Treasury Secretary Bessent described swap lines as a way to “prevent the sale of the US assets in a disorderly way.” Clearly, he is concerned about stress in the Treasury market.

Further, Iran has openly stated that one of its conditions for the safe passage of oil tankers through Hormuz is the payment of a toll or fee in Chinese yuan equal to around $1 per barrel of oil a tanker is carrying. It is rumored that more than 20 countries have already accepted Iran’s new terms. Iran is likely collecting Hormuz toll payments in yuan in a Chinese bank account and then using that yuan to purchase physical gold or Chinese goods and materials, some of which no doubt support Tehran’s war effort and can be shipped overland to Iran via rail connections through Central Asia without much fear of interdiction or interruption.

Japan is reportedly one of them. Tokyo is heavily dependent on imported energy, with roughly 90% of its oil flowing through the Strait of Hormuz. That vulnerability helps explain reports that Japan may even be using its rival’s currency, the Chinese yuan, to meet Iran’s new payment terms and keep vital energy supplies flowing.

We could soon see the petrodollar system give way to a petroyuan system.

Nobody knows exactly how it will all unfold, but it is clear to me that, for many reasons, the Treasury market and the US dollar will be the biggest losers in the Iran war.

The 10-Year Treasury Yield: The Fiat System’s Stress Gauge

The 10-year Treasury yield is perhaps the most important financial benchmark in the global fiat system, as it drives valuations and market trends worldwide. It is widely—and erroneously—regarded as the risk-free rate of return.

The 10-year Treasury yield can be thought of as a key barometer of the US dollar-based fiat system—a critical measure akin to its beating heart.

Bond yields move inversely to bond prices. When bond prices fall, bond yields rise.

A rising 10-year Treasury yield signals trouble for the US dollar because it means investors are selling Treasuries, which pushes up the US government’s borrowing costs. That is why the 10-year Treasury yield is a major pain point for the US government.

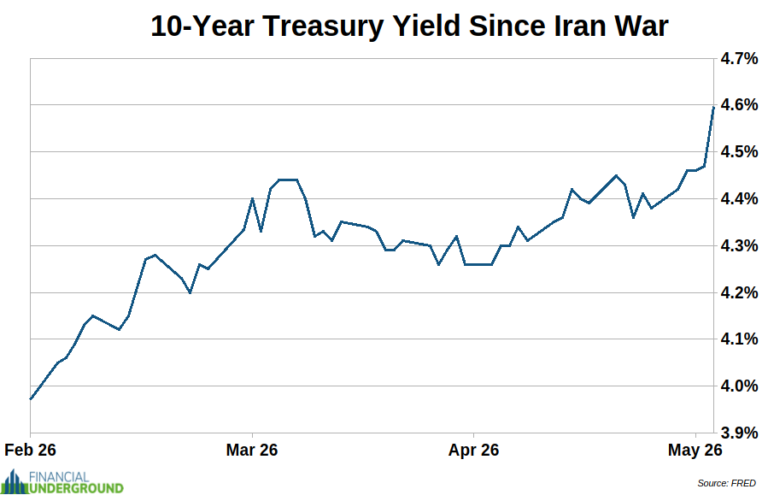

The 10-year Treasury yield was 3.97% when the war started. Now it is around 4.60%, an increase of roughly 63 basis points. 63 bps might not seem like much, but with $39.2 trillion in debt and growing, every basis point matters.

I expect the 10-year Treasury yield to keep climbing over the coming weeks and months—until it forces the Fed’s hand. At that point, the intervention will be sold as “stability,” but the mechanism will be familiar: suppress yields by debasing the currency.

At today’s debt levels, every 1 basis point increase in the government’s average borrowing cost adds roughly $3.9 billion in annual interest expense. So a 63 bps rise is not trivial—it translates to nearly $250 billion in additional yearly interest costs, materially widening a 2025 budget deficit that was already around $1.8 trillion.

Higher yields mean the US government must pay tens or even hundreds of billions more in interest on its debt. At the same time, the global economy faces even greater added costs because Treasury rates serve as the benchmark for borrowing worldwide.

That is not an insignificant move. However, given all the headwinds I have discussed, I suspect the 10-year Treasury yield is headed much higher because investors will demand higher yields to compensate for rising inflation. Further, if Hormuz remains closed, drastically higher oil prices are all but certain. Higher energy prices mean higher prices across the economy and higher official inflation rates, which means investors will demand still higher yields to compensate.

The problem is that interest on the federal debt is already over $1.2 trillion and is now the second-largest item in the budget. The US government cannot afford yields going much higher because the interest expense would push it toward bankruptcy.

I am not sure how—or even if—the US government can manage this situation. Something has to give, and we will not have to wait long to find out what.

The Iran war may prove to be more than another foreign policy disaster. It could be the trigger that exposes the fragility of the entire dollar-based financial system.

When war, debt, inflation, and a weakening Treasury market all collide, the consequences can move faster than most people expect. The mainstream media will not help you see it coming—and by the time it becomes obvious, it will be too late to take action.

That is why I prepared an urgent free report on the dangerous economic, political, and cultural trends now unfolding, the risks they pose to your money and personal freedom, and the three strategies you need to consider right now.